Executive Summary

I would like to thank our clients whose commitment to ARK’s strategies has remained strong during the last few years. As an investor in our funds myself, I understand that volatility can be frustrating and unsettling. Hit disproportionately by the record-breaking interest rate shock in 2022, ARKK, our flagship fund that offers thematically differentiated, nearly pure-play exposure to disruptive innovation, remains 72% below its peak while broad-based benchmarks like the S&P 500—powered by very few stocks—are reaching all-time highs.

Acknowledging fully that the macro environment and some stock picks have challenged our recent performance, I would like to communicate why our conviction in and commitment to investing in disruptive innovation have not wavered. First, in our view, many stocks associated with truly disruptive innovation have settled into rare, deep value territory. Second, if interest rates unwind, we believe ARK’s differentiated disruptive innovation strategies should benefit disproportionately, as they did in the fourth quarter of 2023 and during the coronavirus crisis.

Typically, truly disruptive innovation evolves as agile companies build from scratch, cutting against or undermining the competitive strengths of incumbents. An auto sector that relies upon the sale of auto parts for profitability, for example, is not well-suited to the new manufacturing footprint and lower maintenance costs associated with electric vehicles. Similarly, the massive distribution footprints of traditional drug manufacturers are less relevant as molecular diagnostics point the way to precision therapies tailored to individual patients. What good is a bank branch network—or a bank at all—as peer-to-peer transactions settle between digital wallets? And, what happens to the hundreds of billions of dollars of freight rail assets if autonomous electric trucks can deliver packetized products directly to distribution centers for the same cost per ton mile?

Accelerating all disruptive innovation is artificial intelligence. AI is transforming how software is designed and deployed. AI is likely to shake up, if not destroy, the technological power structure in place today and to reorganize every sector in ways we will not recognize during the next five to ten years.

To harness this massive technological transformation efficiently and effectively, incumbents should scrap their playbooks, but are unlikely to do so. Instead, they may take the “sustaining innovation” path,1 creating better-performing products to sell for higher profits to their best customers while failing to transform their business models or reimagine their products and operations. Such companies are likely to incorporate or cram disruptive technologies into their existing business models, the cashflow-generation machines that have served them well over the last ten to 15 years.

In so doing, they might turn completely new technological platforms into marketing gimmicks—”nice to have” features. In the meantime, high interest rates also have focused investors on short-term cash flow instead of longer-term returns on invested capital.

In our view, investment strategies approaching disruptive and sustaining innovation in the same way will prove short-sighted for two reasons. First, even if interest rates were to stabilize at current levels, strategic investments in disruptive innovation platforms are likely to lead to outsized cash flow yields.2 Expecting high returns on invested capital is key to underwriting and forecasting technologies and associated securities. Tesla is an important case in point.3 Tesla did not turn cash flow positive for nearly a decade after its IPO in 2010. Instead, it invested billions in a vertically integrated EV manufacturing, distribution, and charging platform, which now generates billions in cash flow per year.

Second, marginal changes in interest rates should set investor sights on the potential cash flow generation of disruptive innovation platforms. If interest rates fall, as we anticipate, current cash flows will become relatively less valuable than future cash flows, especially for disruptive platforms, putting at a disadvantage incumbents that try to incorporate disruptive technologies as optional add-ons. Without committing fully to new platforms, incumbents could cannibalize once-healthy business lines, while once-undercapitalized disruptive competitors scale and expand balance sheets to invest aggressively.

Our commitment to disruptive innovation is likely to be supported by two “reversions to the mean” that we believe are in early stages. One such reversion benefited value strategies during 2000, the other platform companies in growth strategies at the end of the tech and telecom bust. Those dynamics convince us that exiting our strategies now would crystallize losses that lower interest rates and reversions to the mean should transform into meaningful profits during the next few years. We are resolute!

ARK’s Strategies: The Market Backdrop

Interest Rates

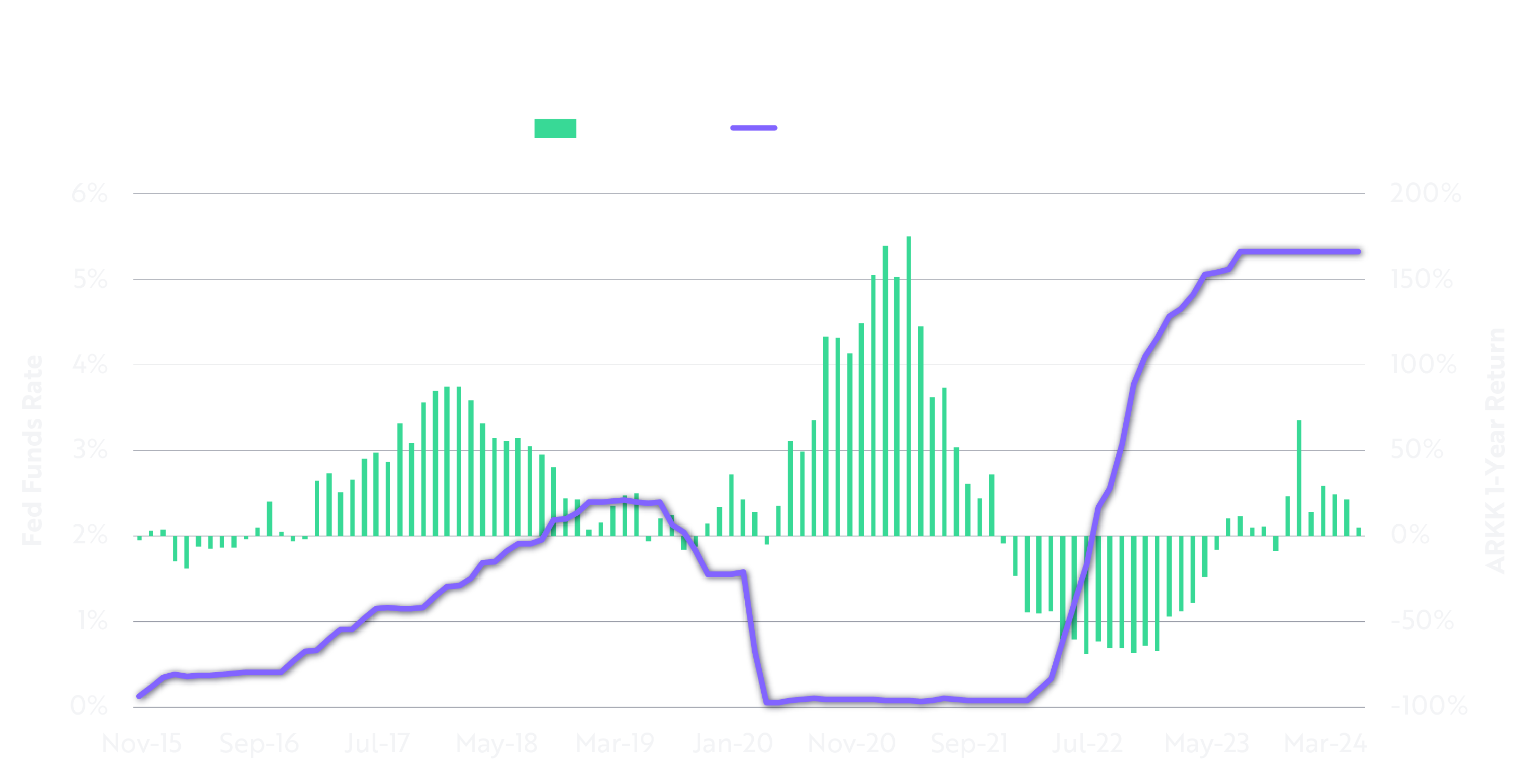

Historically, ARK's relative performance has not been held hostage to interest rate moves one way or the other. ARKK performed very well in 2017 and 2018, for example, when interest rates were rising at a measured rate, as shown below. That said, this market cycle has been exceptional. In a shock to all long-duration assets—including long-term bonds which delivered their worst performance since the 1700s—the U.S. Federal Reserve (Fed) increased target interest rates 22-fold in little more than a year’s time in 2022-2023.

Source: ARK Investment Management LLC, 2024, based on data from Morningstar as of May 31, 2024. For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security. To view the performance of ARKK, visit: https://www.ark-funds.com/funds/arkk.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal will fluctuate so that an investor’s shares when redeemed may be worth more or less than the original cost. Extraordinary performance is attributable in part due to unusually favorable market conditions and may not be repeated or consistently achieved in the future. The Fund’s most recent month-end performance can be found in the fund material section.

Unlike last year, when markets began to anticipate lower interest rates and reward long-duration assets, this year the Fed's mantra changed to "higher for longer" as companies tried to offset faltering unit growth with higher prices. That behavior stalled the improvement in CPI-based4 inflation in the 3-3.5% range and PCE-based5 inflation in the 2.5-2.7% range. Consumers rebelled, however, so now companies like Walmart, Target, Costco, McDonalds, Starbucks, and others are announcing broad-based price declines that should impact both the PPI and CPI. Service-based inflation, particularly shelter, is likely to follow. As a result, the rolling recession that has been in place since the Fed hiked interest rates in 2022—starting with commercial real estate and housing, autos, capital spending, and now consumption—should result in lower-than-expected inflation and interest rates, reigniting the tailwind for long duration assets that began last year.

Equity Market Concentration

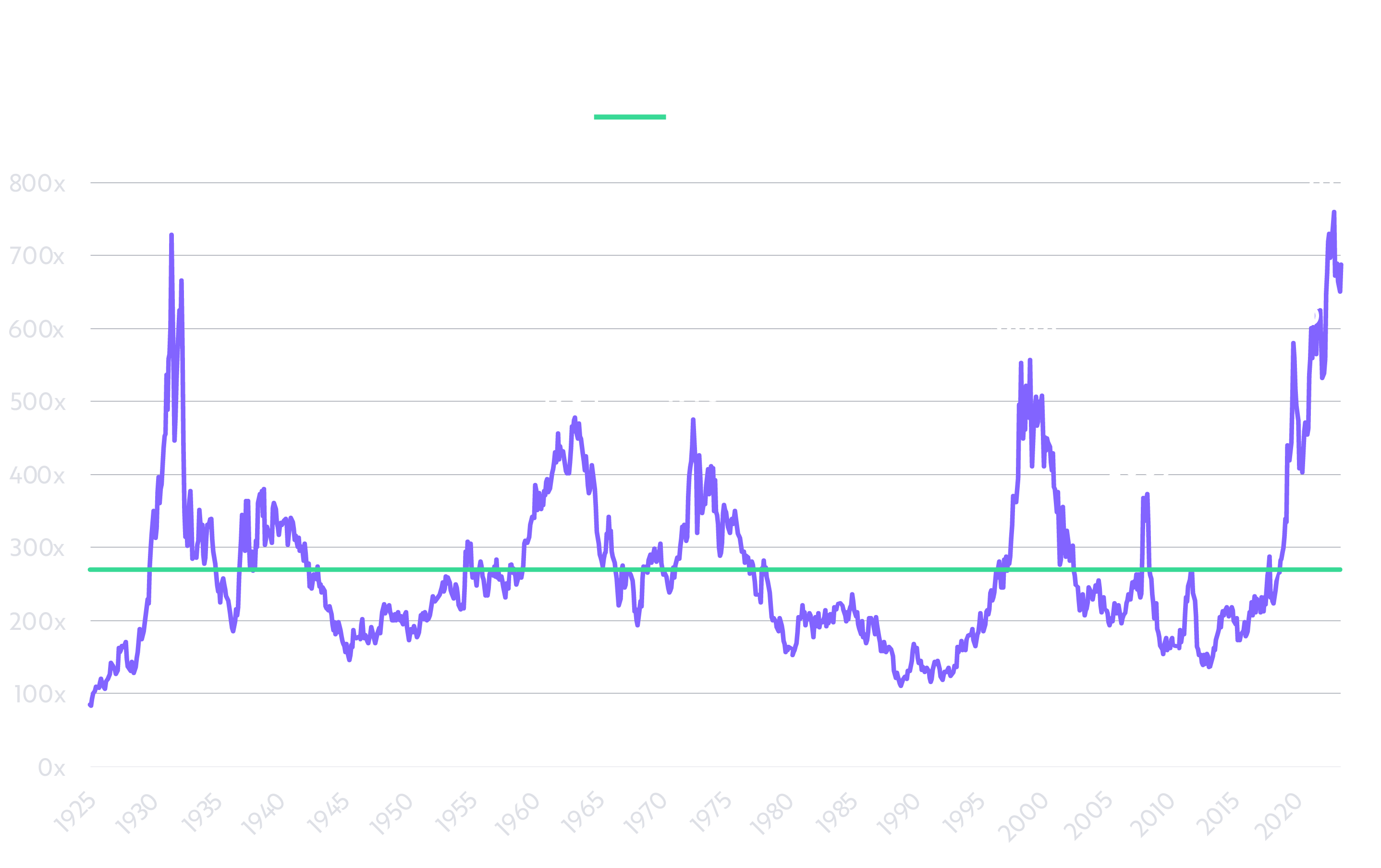

While momentum alone could push concentration in the equity markets back above levels last seen during the Great Depression, the average large cap growth strategy already had more than 45% exposure to the Magnificent Six6 as of May 2024,7 causing the concentration illustrated in the chart below.

Source: ARK Investment Management LLC, 2024, based on data from Macrobond as of May 31, 2024. For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security or cryptocurrency. Past performance is not indicative of future results.

Ironically, in the most stringent anti-trust environment in recent memory, the equity market capitalization has never been more concentrated, as measured by the ratio of the highest market cap stock in the US equity market relative to the 75th percentile stock. In recent months, the concentration surpassed that seen in the Great Depression from 1929 to 1932, during which time the unemployment rate soared to 25%, real Gross Domestic Product (GDP) fell 29%, the wholesale price index dropped 32%, and the consumer price index dropped 25%. Clearly and understandably, in 1932 the market was evaluating companies with a binary filter—bankruptcy or no bankruptcy—based on cash cushion and free cash flow.

In comparison, despite the relatively benign economic environment today, equity markets have behaved similarly, rewarding companies with large cash cushions and free cash flow, in addition to surprising short-term revenue growth associated with “AI.” From our point of view, many of those “AI” opportunities fall into the category of sustained innovation, favoring the data aggregators that capitalized on the first leg of the internet revolution. While perhaps true in the short term, if ARK is correct, the most important AI investment opportunities will be more disruptive, as the most significant technology platform shift in history creates surprising winners and losers, particularly, a more diverse set of winners to which the current equity market concentration should give way.

Two dates in the concentration chart above—1973 and 2000—stand out, because they indicate peaks in the equity market after Fed policy erred on the side of easing. Those narrow markets ended badly. The former sealed the demise of the “Nifty Fifty” like Xerox and Avon Products, while the latter signaled the end of the tech and telecom bubble. In 1973, after the US closed the gold window, monetary policy became unhinged, financed “guns and butter” fiscal policy, and accommodated a quadrupling in oil prices, not to mention generalized commodity price inflation. Equity market valuations went into a tailspin for nearly a decade, pushing the P/E ratio8 of the S&P 500 down from 18.4x in 1972 to 6.7x in 1980. Likewise, by 2000, monetary policymakers had eased consistently in response to the implosion of Long Term Capital Management in 1998, the risks of a global shutdown associated with Y2K at the turn of the Millenium, and the tech and telecom bust in 2000. As a result, the P/E of the Nasdaq 1009 dropped from 200x in 200010 to 30x in 2004, and bottomed at 13x in 2008.11

Today, the risk appears to be the opposite: restrictive monetary policy caused by the Fed’s concern that it let the inflation genie out of the bottle during the COVID crisis. In Chairman Powell’s words, Fed policy is “restrictive.” Unlike in 1973 and 2000 when M212 increased 6.6% and 6.2% on a year-over-year basis, respectively, money growth turned negative and stayed negative on a year-over-year basis from December 2022 through March 2024 and now, at 0.6%, is still extremely weak by historical standards.

Unlike in 1973 and 2000, other peaks in equity market concentration signaled the beginning of broader-based equity bull markets: 1932, 1964, and 2009. From peak concentration in 1932, for example, the S&P 500 appreciated ~269%, or ~9.8% at an annual rate, through 1945 while small caps outperformed large caps by ~13.6% at an annual rate. In the earlier stage of that bull market, from peak concentration in 1932 to the interim low in 1936, small caps outperformed large caps by 23.4% at an annual rate. Both 1964 and 2009 played out similarly, with small caps outperforming large caps by 22.2% at an annual rate in the 1964 cycle and 4.8% from 2009-2013.

In our view, having already paid dues with tight money and higher interest rates in this cycle, the next few years could prove fertile for a broad swath of the equity market beyond the Magnificent Six. While mega-cap stocks should participate in a broad-based bull market, we believe smaller-cap stocks will have much more compelling upside potential.

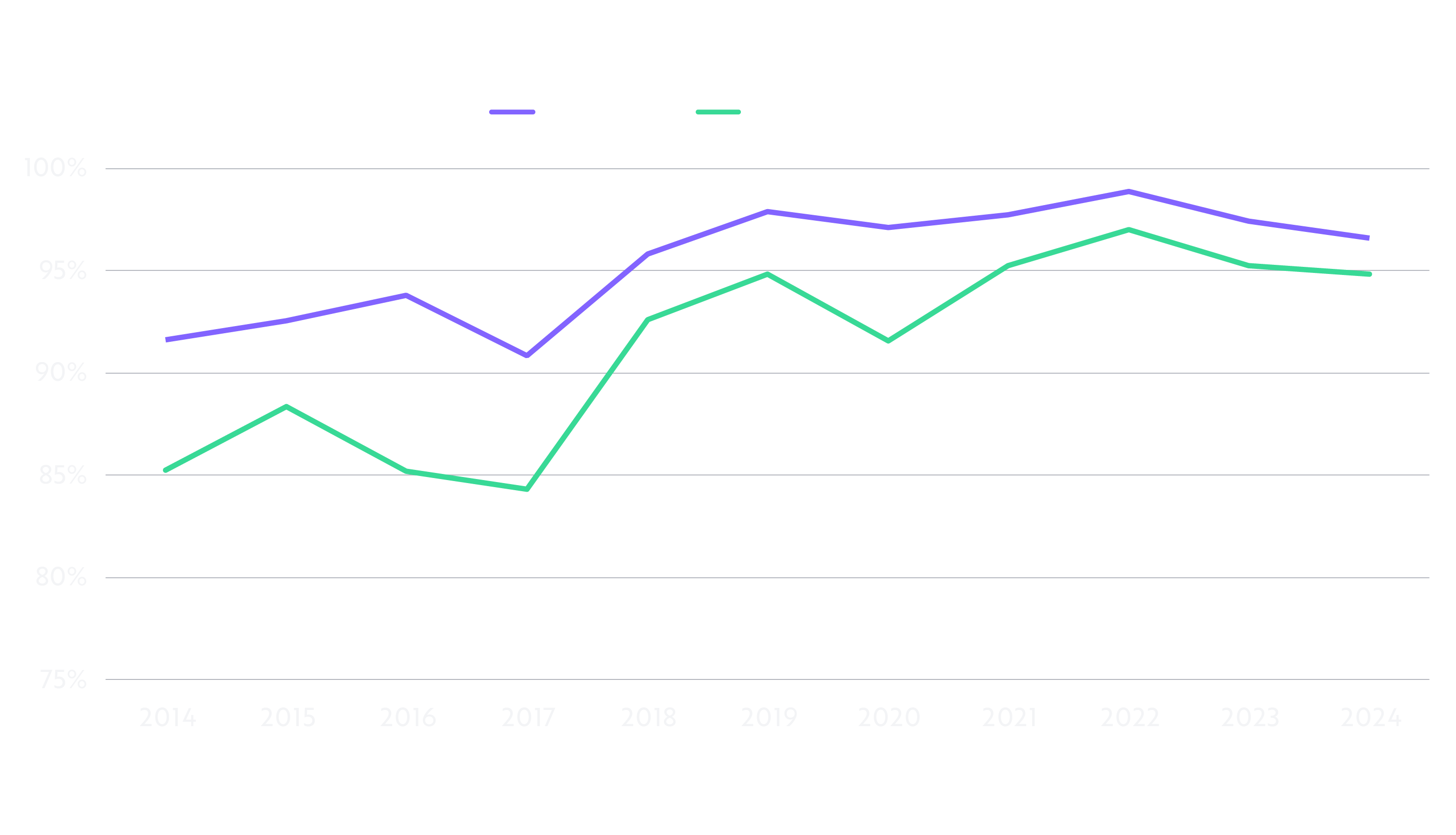

To help investors understand our value proposition, ARK Invest describes its all-cap strategy as the closest to a venture capital fund in the public equity markets. ARK offers diversified and differentiated exposure to truly disruptive innovation. The five innovation platforms upon which we have focused our research and investing—robotics, energy storage, artificial intelligence, blockchain technology, and multiomics sequencing—are converging. Many of our stocks are not in benchmarks and therefore are not well understood or covered by buy-side and sell-side research. Yet, we believe those inefficiently priced stocks will benefit enormously. For this reason, ARKK’s exposure to the Magnificent Six as of May 2024 was 2%, compared to the 30% in the S&P 500 and 39% in the Nasdaq 100. Since inception on October 31, 2014 through May 31, 2024, ARKK’s active share13 relative to the S&P 500 and to the Nasdaq 100 has averaged ~95% and ~91%, respectively, as shown below.

Source: ARK Investment Management LLC, 2024, based on data from Morningstar as of May 31, 2024. For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security. Indexes are unmanaged and are not available for direct investment.

What About Nvidia?

Nvida’s performance has been exceptional, and the stock has been an important contributor to ARK’s and ARKK’s performance since inception in October 2014. Indeed, NVDA has been the fifth largest contributor to ARKK’s performance. Early on, we identified Nvidia as the premier “picks and shovels” play in the AI space. In addition, our ARK Next Generation Internet ETF (ARKW)—focused primarily on AI, cloud computing, and digital assets—remains exposed to NVDA, with a 1.39% weight as of June 28, 2024.

In late 2022, Nvidia, the primary provider of accelerated systems that power generative AI, began to price in the impact of OpenAI’s “ChatGPT moment.” By that time, the Fed was well-advanced in its 22-fold hike in interest rates, which hit economic activity and weakened many stocks in ARKK. As investors plowed into NVDA and the other cash rich Magnificent Six stocks, the equity market hit record-breaking levels of concentration, spurring our search for diversified exposure to the AI revolution, particularly the software applications that our research suggests are underrepresented in broad-based benchmarks but likely to drive value creation during the next five years.

Since then, a weak macro environment and longer-term corporate strategic decision-making have challenged software companies. AI deployments have not bolstered corporate revenues, productivity, and/or margins as significantly as our research suggests they ultimately will. Given high and perhaps unfulfilled short-term expectations, customers are likely to reassess their AI strategies, causing Nvidia’s business some short-term indigestion. In addition, competitors—including some of Nvidia’s own customers—are aiming to gain share in the AI accelerator market with “good enough” supply at lower prices and margins.

That said, we view artificial intelligence as a foundational innovation platform that will serve as a launching pad for many technologies and many new companies. We invest across the full AI stack, from chips to cloud platforms to highly converged AI applications, believing it important for investors to have exposure to this spectrum of AI opportunities, not just the layer capturing outsized attention today.

Valuation And Reversions To The Mean: Analogies To The Tech And Telecom Bubble And Bust

During the tech and telecom bubble, too much capital chased too few opportunities, as the technologies were not ready for prime time and/or their costs were prohibitive. For investors and many companies, the tech and telecom bubble ended badly. That said, the seeds for the five innovation platforms around which ARK has centered its research—robots, energy storage, artificial intelligence, blockchain technology, and multiomics sequencing—were planted during the 20 years that ended in the tech and telecom bubble and have been germinating for the last 25-40 years.

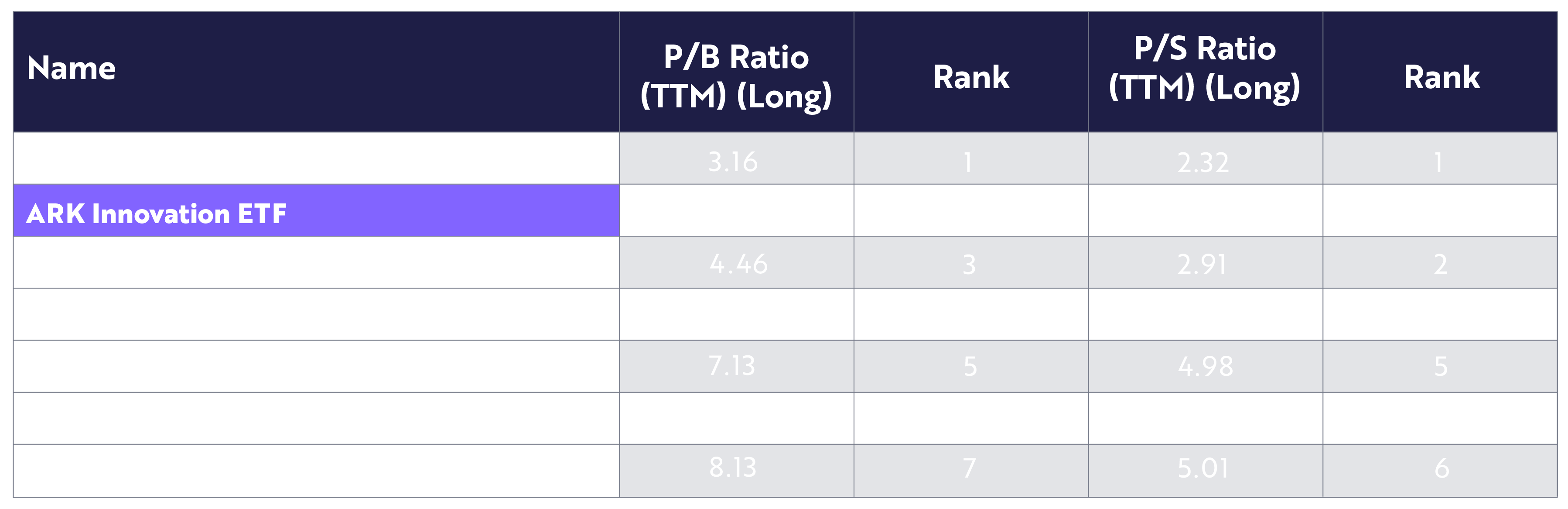

Unlike in 2000, the Nasdaq 100 and the S&P 500 today look very similar, their number of common holdings now at 84, representing 95% of the Nasdaq 100’s cumulative weight and 49% of the S&P 500’s cumulative weight as of June 30, 2024. Their valuations are not much different either, as measured by adjusted enterprise value (EV)14 to EBITDA15—20.7x and 22.2x, respectively. Interestingly, the adjusted EV to EBITDA of our flagship strategy, ARKK, was 25.5x as of June 2024, the lowest premium to either of the more mature broad-based indices in my memory, and well below its peak valuation of 94x in February 2021.16

With this low a valuation at a time when disruptors are sacrificing short-term profitability and investing aggressively, ARKK seems to have entered deep value territory based on our five-year investment time horizon. In early 2016, our first institutional client appreciated ARK’s contrarian and “value-oriented” approach to investing in disruptive innovation, particularly our focus on underappreciated names. Suggesting the same and perhaps more surprising are valuations based on Price-to-Book (P/B)17 and Price-to-Sales (P/S),18 as shown in the table below.

Source: ARK Investment Management LLC, 2024. Based on data from Morningstar as of May 31, 2024. For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security. Past performance is not indicative of future results. Indexes are unmanaged and are not available for direct investment. Please note the following specifications for the categories used in the table above: “TTM” – Trailing Twelve Months. “Long” – Long positions in the portfolio. The categories shown are Morningstar categories. The ARK Innovation ETF is considered a Mid-Cap Growth Fund per Morningstar. While ARKK is not listed in the US Fund Technology or US Fund Large Growth Categories by Morningstar, we list these comparisons, as they hold the names that the indexes have concentrated into as shown previously. “P/B” – The weighted average of the price/book ratios of all the stocks in a portfolio. The P/B ratio of a company is calculated by dividing the market price of its stock by the company’s per-share book value. Stocks with negative book values are excluded from this calculation. In theory, a high P/B ratio indicates that the price of the stock exceeds the actual worth of the company's assets, while a low P/B ratio indicates that the stock is a bargain. All P/B ratios greater than 75 are capped at 75 for the calculation. “P/S” – Represents the weighted average of the price/sales ratios of the stocks in a portfolio. Price/sales represents the amount an investor is willing to pay for a dollar generated from a particular company's operations.

The approach has worked against our performance this year, as ARKK reduced exposure to the Magnificent Six and increased exposure to multiomics stocks that have been hit hardest by “higher for longer” interest rates. Unlike the S&P 500, which has hit all-time highs, ARKK today is 72% below its peak and ARKG, 78%, another illustration of deep value territory.

Important to recognize, however, is that in 2023 ARKK appreciated 68% as the bull market started to broaden out based on just the “whiff” of lower interest rates, despite its diversification away from the Magnificent Six and toward what we believe are more disruptive names like Coinbase, Palantir, Roku, Tesla, Draftkings, UiPath, Shopify, Crispr Therapeutics, Twist, and 10X Genomics. ARKK outperformed the Nasdaq 100 by 1300 basis points19 and the S&P 500 by 4100 basis points, a harbinger we believe of a broader-based and healthier equity market as interest rates decline in the years ahead.

The Tech And Telecom Bubble

To reiterate, after paying significant dues during the unprecedented interest rate shock in 2022, ARK’s strategies seem to have entered deep value territory in the context of a five-year investment time horizon. A look back at the performance of value vs. growth during another “extreme” period in history illustrates how suddenly a tightly coiled spring aimed in the right direction can transform relative performance.

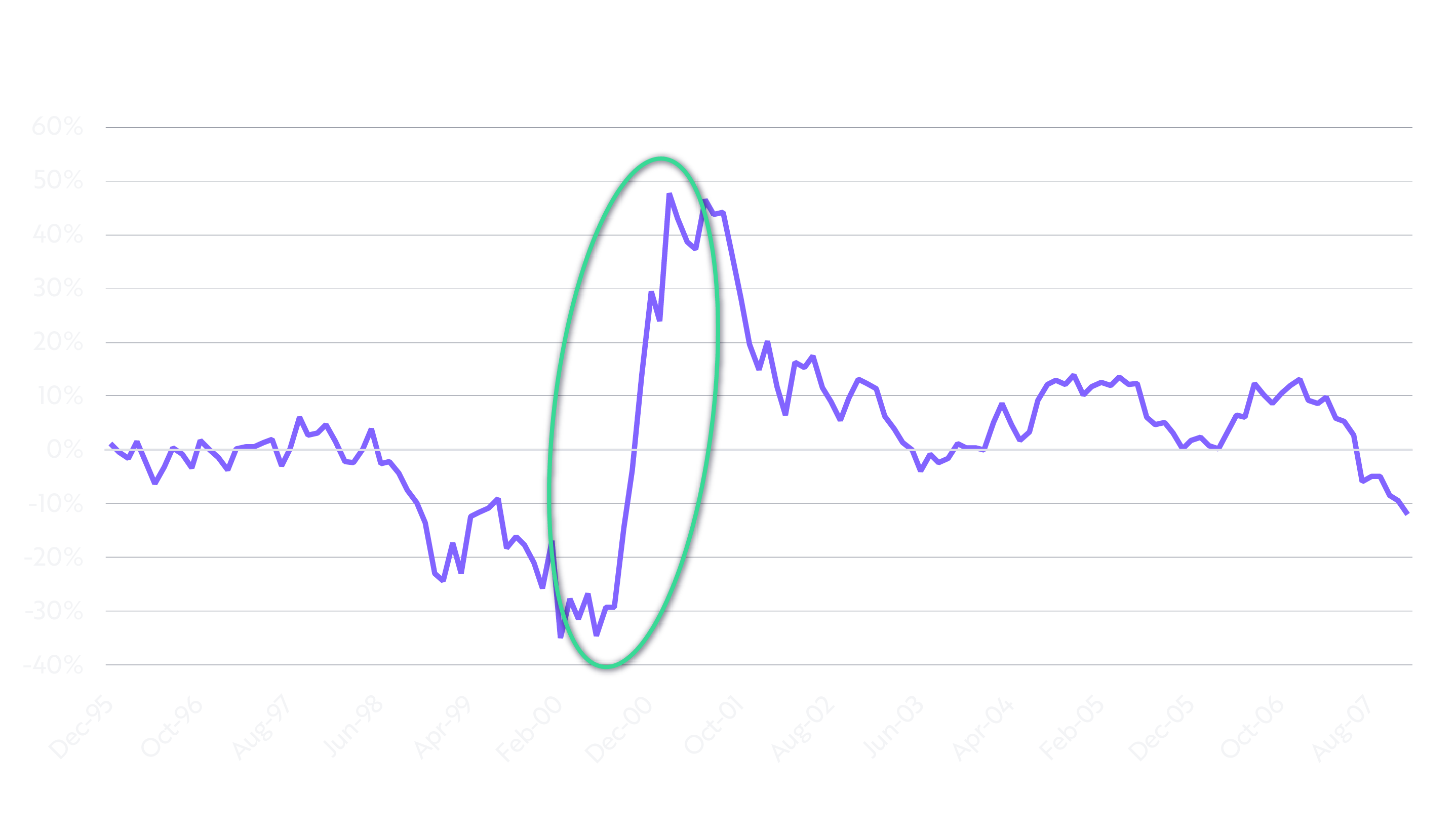

During the late nineties, value strategies as measured by the Russell 1000 Value index20 underperformed growth strategies on a year-over-year basis for roughly two and a half years. At a painful time for all value managers, Sanford C. Bernstein, a premier US value manager, agreed to sell its business to Alliance Capital, a premier US growth manager, near the nadir of its relative performance. At its worst in 2000, the Russell Value Index underperformed the Russell Growth Index by more ~3500 basis points on a year-over-year basis but, within roughly one year, the relative performance flipped and reached a positive ~4800 basis points, more than an 80-percentage point swing, as shown below.

Source: ARK Investment Management LLC, 2024, based on data from Morningstar as of 12/31/2007. For informational purposes only and should not be considered investment advice or a recommendation to buy, sell, or hold any particular security. Indexes are unmanaged and are not available for direct investment.

The Tech And Telecom Bust

Recent performance has been extremely challenging, reminding me of an important moment in the tech and telecom bust. In 2002-03, most buy-side and sell-side had turned tail on anything that smacked of the dot-com bubble. At a prior firm, my team bought AMZN (Amazon) at an enterprise value of ~$5 billion. While we thought online retail was a big idea, most observers considered the internet a figment of Wall Street’s wild imagination during a bubble and assumed that it would never be profitable. Since then, and in response to the company’s willingness to sacrifice short-term profitability for long-term gain until 2003, AMZN has appreciated 29.8% at an annual rate, hitting ~$2 trillion in market cap.

Similarly, in the multiomics space today, Pacific Biosciences (PACB) and Crispr Therapeutics (CRSP) are two platform companies in the long-read sequencing and gene-editing spaces, respectively, that are sacrificing short-term profitability for potential long-term gain. At an early stage, both are “burning cash” as they invest in ways that we believe will enable them to dominate their spaces, each of which could deliver growth rates above 30% at an annual rate during the next five to ten years. Unfortunately, in the short term, algorithmic trading—which according to some estimates21 accounts for 60-75% of daily trading in the US—seems focused on little other than current quarter revenue growth, cash cushion, and cash burn.22

After dropping 97% and 73% from their peaks in 2021, respectively, the enterprise value of Pacific Biosciences (PACB) is $742 million and that of Crispr Therapeutics (CRSP), $2.7 billion, as of June 28, 2024, representing two of the most undervalued stocks in our portfolios. As Pacific Biosciences contributes to diagnosing diseases like cancer at or before Stage 1, and as Crispr Therapeutics cures sickle cell disease and, in the future perhaps, diabetes, both PACB and CRSP appear to me to be in a position like that of Amazon in 2003. Indeed, in our view, the focus on benchmark-style investing has created more severe undervaluation of stocks in the disruptive innovation space today than in 2003.

Conclusion: ARK’s Value Proposition

Even if we are wrong that inflation and interest rates are poised to surprise on the low side of expectations, ARK’s strategies, beginning with ARKK, have paid the dues associated with higher interest rates and are offering a highly differentiated exposure to innovation, especially given record-breaking mega-cap concentration in the US equity market juxtaposed against bargain basement valuations in small- to large-cap equities in the disruptive innovation space. If inflation and interest rates do surprise on the low side of expectations, much like the equity market began to discount last year, that tailwind could reward equities focused on truly disruptive innovation disproportionately.

Important Information

Investors should carefully consider the investment objectives and risks as well as charges and expenses of an ARK Fund before investing. This and other information are contained in the ARK ETFs’ and ARK Venture Fund’s prospectuses, which may be obtained by visiting www.ark-funds.com and www.ark-funds.com/funds/arkvx, respectively. The prospectus should be read carefully before investing.

An investment in an ARK Fund is subject to risks and you can lose money on your investment in an ARK Fund. There can be no assurance that the ARK Funds will achieve their investment objectives. The ARK Funds’ portfolios are more volatile than broad market averages. The ARK Funds also have specific risks, which are described below. More detailed information regarding these risks can be found in the ARK Funds’ prospectuses.

The principal risks of investing in the ARK Funds include:

Disruptive Innovation Risk. Companies that ARK believes are capitalizing on disruptive innovation and developing technologies to displace older technologies or create new markets may not in fact do so. Companies that initially develop a novel technology may not be able to capitalize on the technology. Companies that develop disruptive technologies may face political or legal attacks from competitors, industry groups or local and national governments. These companies may also be exposed to risks applicable to sectors other than the disruptive innovation theme for which they are chosen, and the securities issued by these companies may underperform the securities of other companies that are primarily focused on a particular theme.

Equity Securities Risk. The value of the equity securities the ARK Funds hold may fall due to general market and economic conditions. Foreign Securities Risk. Investments in the securities of foreign issuers involve risks beyond those associated with investments in U.S. securities. Health Care Sector Risk. The health care sector may be affected by government regulations and government health care programs. Consumer Discretionary Risk. Companies in this sector may be adversely impacted by changes in domestic/international economies, exchange/interest rates, social trends and consumer preferences. Industrials Sector Risk. Companies in the industrials sector may be adversely affected by changes in government regulation, world events, economic conditions, environmental damages, product liability claims and exchange rates. Information Technology Sector Risk. Information technology companies face intense competition, both domestically and internationally, which may have an adverse effect on profit margins.

Financial Technology Risk. Companies that are developing financial technologies that seek to disrupt or displace established financial institutions generally face competition from much larger and more established firms. Fintech Innovation Companies may not be able to capitalize on their disruptive technologies if they face political and/or legal attacks from competitors, industry groups or local and national governments. Blockchain technology is new and many of its uses may be untested. Blockchain and Digital commodities and their associated platforms are largely unregulated, and the regulatory environment is rapidly evolving. As a result, companies engaged in such blockchain activities may be exposed to adverse regulatory action, fraudulent activity or even failure. Communications Sector Risk. Companies is this sector may be adversely affected by potential obsolescence of products/services, pricing competition, research and development costs, substantial capital requirements and government regulation.

Cryptocurrency Risk. Cryptocurrency (notably, bitcoin), often referred to as ‘‘virtual currency’’ or ‘‘digital currency,’’ operates as a decentralized, peer-to-peer financial exchange and value storage that is used like money. Some of the ARK actively managed Funds may have exposure to bitcoin, a cryptocurrency, indirectly through an investment in the ARK 21Shares Bitcoin ETF, a 1933-Act exchange traded product. Cryptocurrency operates without central authority or banks and is not backed by any government. Even indirectly, cryptocurrencies may experience very high volatility and related investment vehicles like ARKB may be affected by such volatility. As a result of holding cryptocurrency, the Fund may also trade at a significant premium to NAV. Cryptocurrency is also not legal tender. Federal, state or foreign governments may restrict the use and exchange of cryptocurrency, and regulation in the U.S. is still developing. Cryptocurrency exchanges may stop operating or permanently shut down due to fraud, technical glitches, hackers or malware. Leverage Risk. The use of leverage can create risks. Leverage can increase market exposure, increase volatility in the Fund, magnify investment risks, and cause losses to be realized more quickly.

Additional risks of investing in ARK ETFs include market, management and non-diversification risks, as well as fluctuations in market value NAV. ETF shares may only be redeemed directly with the ETF at NAV by Authorized Participants, in very large creation units. There can be no guarantee that an active trading market for ETF shares will develop or be maintained, or that their listing will continue or remain unchanged. Buying or selling ETF shares on an exchange may require the payment of brokerage commissions and frequent trading may incur brokerage costs that detract significantly from investment returns.

Index Descriptions: The S&P 500 is a stock market index tracking the stock performance of 500 of the largest companies listed on stock exchanges in the United States. The Nasdaq 100 Index is a stock market index made up of 101 equity securities issued by 100 of the largest non-financial companies listed on the Nasdaq stock exchange.

“Fed” refers to the U.S. Federal Reserve, the central banking system of the United States.

Fed Funds Rate is the interest rate at which depository institutions (banks and credit unions) lend reserve balances to other depository institutions overnight on an uncollateralized basis.

Gross Domestic Product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period. Nominal GDP is a measure of economic output that uses current prices and does not adjust for inflation. Real GDP is an economic metric that is used to describe the economic output of a country within a specific year. It reflects the value of all goods and services produced while factoring inflation into its calculation.

The “Nifty Fifty,” as referenced in this material, was a group of 50 large-cap stocks on the New York Stock Exchange that were most favored by institutional investors in the 1960s and 1970s. Investment in these top 50 stocks—similar to blue-chip stocks of today—is said to have propelled the American economy to its bull market of the 1970s.

"Guns and Butter," as referenced in this material, describes the government allocation to defense spending versus social programs.

“Y2K,” or the year 2000, refers to potential computer errors related to the formatting and storage of calendar data for dates in and after the year 2000. Many programs represented four-digit years with only the final two digits, making the year 2000 indistinguishable from 1900. Contrary to published expectations, few major errors occurred in 2000.

Market capitalization, or "market cap," represents the total dollar market value of a company's outstanding shares of stock. Small-cap companies are those with a market cap between $250 million and $2 billion. Large-cap companies are those with a market cap of more than $10 billion. Mega-cap companies are those with a market cap of more than $200 billion.

ARK Investment Management LLC is the investment adviser to the ARK Funds.

Foreside Fund Services, LLC, distributor.

Cote, C. 2022. “Sustaining vs. Disruptive Innovation: What's the Difference?” Harvard Business School. For the example of Kodak, see DiSalvo, D. 2011. “The Fall of Kodak: A Tale of Disruptive Technology and Bad Business.” Forbes.

Cash flow, in general, refers to payments made into or out of a business, project, or financial product. It also may refer to the real or virtual movement of money.

Please view ARKK’s top ten holdings here: https://www.ark-funds.com/funds/arkk.

Consumer Price Index. The Consumer Price Index measures the overall change in consumer prices based on a representative basket of goods and services over time.

Personal Consumption Expenditures. Personal consumption expenditures is a measure of consumer spending and includes all goods and services bought by US households.

The Magnificent Six or “Mag 6” stocks are a group of high-performing and influential companies in the US stock market: Alphabet, Amazon, Apple, Meta Platforms, Microsoft and NVIDIA.

According to Morningstar as of May 31, 2024.

The Price to Earnings Ratio or P/E Ratio is calculated by dividing the market value price per share by the company's earnings per share (EPS).

The Nasdaq 100 Index is a stock market index made up of 101 equity securities issued by 100 of the largest non-financial companies listed on the Nasdaq stock exchange.

Shafer, B. 2023. “Are Stocks In A Bubble?” The Motley Fool.

Based on data from Bloomberg.

M2 is a measure of the US money stock that includes M1 (currency and coins held by the non-bank public, checkable deposits, and travelers’ checks) plus savings deposits (including money market deposit accounts), small time deposits under $100,000, and shares in retail money market mutual funds.

Active Share is a measure of the percentage of stock holdings in a manager's portfolio that differs from the benchmark index.

Enterprise value (EV) is a company's total value, often used as a more comprehensive alternative to market capitalization.

EBITDA, or earnings before interest, taxes, depreciation, and amortization, is a financial metric used to measure a company's profitability and operational performance.

The ARK Adjusted EV/EBITDA ratio is calculated by adding expenses related to R&D and stock-based compensation (SBC) back into the EBITDA in order to show what a company’s EBITDA would be if it stopped making voluntary investments and focused on profitability. Specifically, the formula is the following: Enterprise Value / (EBITDA + R&D Expense + All Stock Based Compensation Expense – R&D Stock Based Compensation Expense). One caveat to this calculation: while most companies delineate stock-based compensation expenses related to R&D, some do not, which can lead to some duplication of R&D SBC being added back to the EBITDA, since R&D SBC is already included in the “R&D Expense” figure as well as the “All Stock Based Compensation Expense” figure. This is done consistently for both the calculation of ARK’s funds and related benchmarks. The calculation is weighted average using period end portfolio weights and uses trailing-12-month GAAP financials that are not adjusted prior to ARK’s calculation. Names that have a negative ARK Adjusted EV/EBITDA ratio are removed from the weighted average calculation as not to decrease the total fund ratio artificially. The data are pulled from Bloomberg and assume completeness of reported financials.

The price-to-book (P/B) ratio considers how a stock is priced relative to the book value of its assets.

The price-to-sales ratio (Price/Sales or P/S) is calculated by taking a company's market capitalization (the number of outstanding shares multiplied by the share price) and dividing it by the company's total sales or revenue over the past 12 months.

A basis point (bp) is a unit of measurement that represents 1/100th of 1%, or 0.01%, of a percentage.

The Russell 1000 Value Index measures the performance of the large-cap value segment of the US equity universe. It includes those Russell 1000 companies with relatively lower price-to-book ratios, lower I/B/E/S forecast medium term (2 year) growth, and lower sales per share historical growth (5 years).

Groette, O. 2024. “What Percentage of Trading Is Algorithmic? (Algo Trading Market Statistics).” Quantified Strategies.

Although a full discussion of this topic is beyond the scope of this letter, we believe not only that algorithmic trading has punished stocks with low cash reserves while interest rates are high, but also that they are likely to take the opposite side if and when interest rates are cut.

ARK’s statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. ARK and its clients as well as its related persons may (but do not necessarily) have financial interests in securities or issuers that are discussed. Certain of the statements contained may be statements of future expectations and other forward-looking statements that are based on ARK’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied in such statements.

Explore ARK Funds

Featured Funds:

ARK Trade Notifications

ARK offers fully transparent Exchange Traded Funds (“ETFs”) and provides investors with trade information for all actively managed ETFs.