ARKK Is Trading As Though Fundamentals Do Not Matter

This article was authored in collaboration with ARK’s Associate Portfolio Managers, Sam Korus and Nick Grous, ARK’s Client Portfolio Specialist, Dan White, and ARK’s Assistant Trader, Julian Falcioni.

SUMMARY

We believe the dreams associated with the tech and telecom bubble more than 20 years ago are turning into reality today; yet, the ARK Innovation ETF (ARKK) and our other disruptive innovation funds have been crushed, apparently by fears of another tech and telecom bust. In fact, the decline has been more severe during the last 15 months than for the Nasdaq 15 months after its peak on March 10, 2000. ARK critics are suggesting that the rebound from this bear market will be muted and will take years.

In our view, the bet against disruptive innovation today will prove as ill-informed and ill-timed as purchases of tech and telecom stocks in the late 1990s. Moreover, if our research on the genomic revolution, adaptive robotics, energy storage, artificial intelligence, and blockchain technology is even half right, we believe their exponential growth will propel the companies associated with those platforms forward at remarkable speed during the next five years.

Anyone in the asset management business during the late nineties will remember the fraud associated with “research,” particularly sell-side or broker research during the tech and telecom bubble. Analysts and investors seemed to be valuing stocks based on the number of eyeballs around the world that might view websites at some distant point in the future. In emails that the New York Attorney General surfaced and exposed in 2002, Merrill Lynch analyst Henry Blodget privately described companies that he and other sell-side analysts were recommending as “junk”, “crap”, “powder keg”, and “piece of ____”.[1] Henry was banned from the securities industry for life.

Today, analysts and investors seem laser-focused not on potential eyeballs but on the backward-looking benchmarks against which they are measured and current quarter results. They do not seem to be focused on the long-term growth prospects of companies sacrificing short-term profitability to invest aggressively and capitalize on some of the most profound innovation platforms in history. Fixated on the “tough comps” that many digital and genomics companies faced after the coronavirus crisis, they seem to be assuming that “reversion-to-the-mean” will doom growth rates for the next few years. In contrast to their giddy behavior in the late nineties, investors seem cautious, if not afraid. As measured by the latest BofA Fund Manager Survey,[2] for example, cash levels have not been as high since 2001.

In this piece, we highlight major differences between the late nineties and today. Most important, our research is based on first principles, which we share freely and widely to educate not only investors but also students, parents, and grandparents who are vitally interested in understanding how dramatically innovation is going to transform their lives, their assets, and the world. Critical to our research is understanding the technologies and their costs: contrary to the nineties, our research indicates that the technologies involved in our five innovation platforms are ready for prime time, with costs low enough to allow scaling for mass market expansion.

We will continue to share our research and models to fill a void that we believe is plaguing traditional financial research and to highlight the exponential growth trajectories of the five innovation platforms around which we have centered our research. We welcome you to battle test our research and models. We strive to shine a light on what we believe are the biggest opportunities neglected by benchmark-sensitive asset managers and one of the most massive misallocations of capital in history.

INTRODUCTION

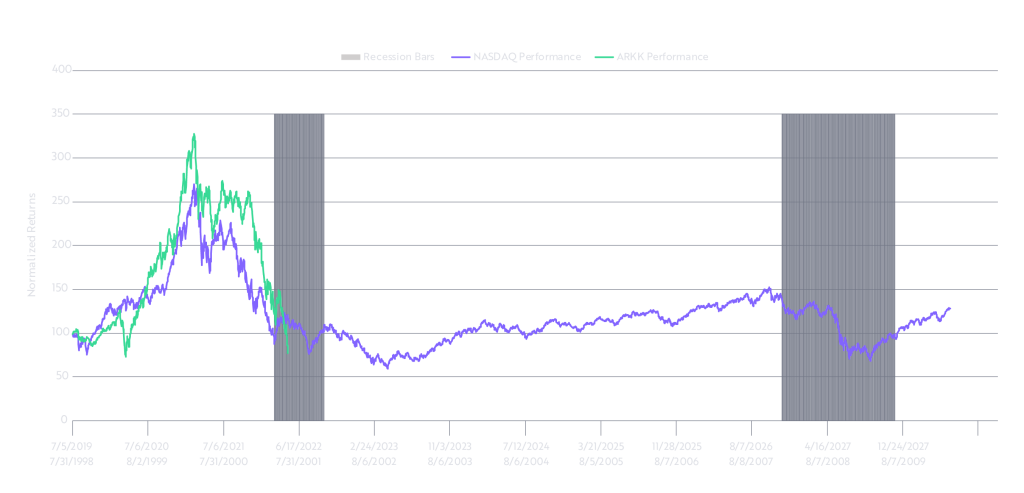

During the past year, critics have compared ARKK’s price action to that of the Nasdaq during the tech and telecom bubble/bust in the late nineties/early 2000s. In our view, algorithms, technicians, and investors in passive ETFs have incorporated little fundamental company and technology research into their analyses. Indeed, some strategies seem to be doing little more than mimicking the behavior of the Nasdaq in 2000-2001 or shorting ARKK based on near-term valuations and betting against innovation. Moreover, during the past year, in response to rising inflation and interest rates, benchmark-sensitive “active” strategies seem to have sold non-benchmark stocks–especially long-duration stocks–to “diversify” back toward their benchmarks. Effectively, they have shorted innovation, pushing equities associated with disruptive innovation into what we believe is deep value territory.

Source: ARK Investment Management LLC, Bloomberg.

Note: The chart was constructed by aligning the peak of the Nasdaq index on 3/10/2000 with the peak price of ARKK on 2/12/2021. Data as of 5.12.22. Data is normalized.

Forecasts are inherently limited and cannot be relied upon.

For informational purposes only and should not be considered investment advice, or a recommendation to buy, sell or hold any particular security.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal will fluctuate so that an investor’s shares when redeemed may be worth more or less than the original cost. Extraordinary performance is attributable in part due to unusually favorable market conditions and may not be repeated or consistently achieved in the future. The Fund’s most recent month-end performance can be found in the fund material section.

Click here for standardized fund performance https://ark-funds.com/funds/arkk/

In a comparison of the revenue, profitability, and long-term valuation of their underlying companies, the Nasdaq circa 2000 and ARKK today bear little resemblance to one another. Interestingly, the Nasdaq Composite’s records are incomplete for the years 2000 to 2003, obfuscating the number of bankruptcies and forced mergers associated with companies that never should have gone public. Acting on euphoria, not fundamental analysis, investors valued companies based on the number of “eyeballs” they ultimately might be able to attract, nothing more. Without 2001-2003 data for the broader index, to compare the Nasdaq of 1998-2005 to ARKK in 2019-2026,[3] we defaulted to the Nasdaq 100, which presumably has benefited from “survivor bias” — stronger revenue growth, higher profitability, and larger capitalizations — relative to the all-cap Nasdaq Composite.

Shares of innovative companies that are bringing to life dreams from the tech and telecom bubble — many of which solved pressing problems during the coronavirus crisis — have collapsed. Many are lower today than at the depths of the coronavirus crisis and even lower than the overlay against the Nasdaq at this point during the bust in 2001.

Based on our research, history may deem this collapse in disruptive innovation shares as more ill-informed and speculative than the bubble during the late nineties. Chasing the dream from 1998 through 2002 ended badly. In our view, running from the reality of disruptive innovation today into value traps — “cheap for a reason” — that increasingly are populating broad-based benchmarks also will end badly. Based on our expectations for the growth trajectories of companies involved in the five major innovation platforms, as discussed below, the price recovery of public equities focused on disruptive innovation will be swift, much shorter in duration than the 15+ year recovery for the Nasdaq 100 after the tech and telecom bust.

INVESTOR MINDSET: 2000-2001 vs 2021-2022

Before comparing the revenue growth and profitability of companies in the Nasdaq 100 circa 2000 and ARKK during the past year, let’s step back and understand a little more about investor psychology in both periods. I remember the unbridled enthusiasm unleashed by the internet and “personalized medicine” in the late nineties. Stoked by three events that caused surges in monetary stimulus — Russia’s default on its ruble-denominated debt in 1998, Long-Term Capital Management’s (LTCM’s) collapse not long thereafter, and “Y2K” fears that global computing would not be able to transition from 1999 to 2000 — investors scrambled to outperform one another with technology exposures higher than the S&P 500’s 33.6%, if not the Nasdaq 100’s 84%. Unfortunately, the technologies that would lead to cloud computing, artificial intelligence, energy storage, industrial robotics, genomic sequencing, and digital cash were not ready for prime time and, even if they had been, their costs would have been too high to enable mass-market adoption. The cost to sequence the first whole human genome, for example, was $2.7 billion at that time, including 13 years[4] of computing power. Deep learning, which today powers GPT-3[5] and other cutting edge AI models, was not viable then because of the high cost and limited scale of computing resources. Nonetheless, too much capital chased too few opportunities too soon, “buying the dip” and the dream throughout 2000 and 2001, which turned into a nightmare.

Today, according to our research, the technologies are ready for prime time, their costs having collapsed––$500 to sequence a whole human genome in a few hours––and yet investors are running for the hills, their benchmarks. In fact, according to a recent BofA fund manager survey,[6] after selling the sector on rallies for a year, investors were more underweight technology in February than they had been since 2006. Currently, the S&P 500’s tech weighting is 27% and the Nasdaq 100’s, 50.5%.[7]

Given the massive amount of disruptive innovation now underway––genomic sequencing, adaptive robotics, energy storage, artificial intelligence, and blockchain technology––the “risk-off” move back to “tried and true” benchmarks that, in our view, will be victims of creative destruction seems fear-driven and short-term focused.

REVENUE AND GROSS PROFITS: 2000-2001 vs 2021-2022

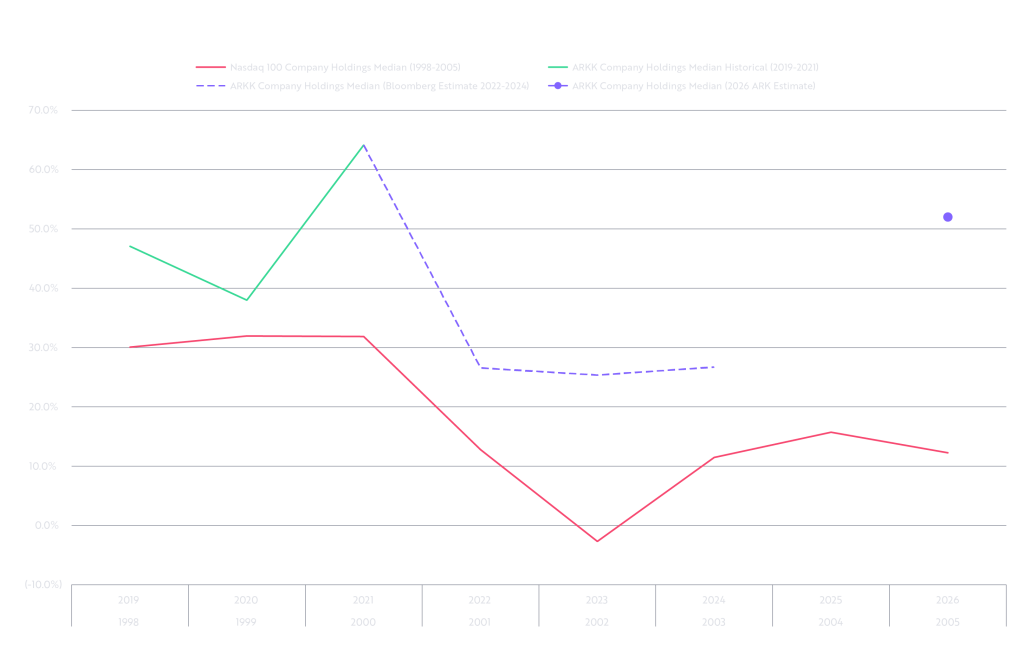

Last year, companies in ARKK increased revenues at more than a 60% rate, roughly twice the rate of those in the Nasdaq 100 as the bubble burst in 2000, as shown below. Among the reasons for the outsized growth were the innovative solutions they provided during the coronavirus crisis: genomic sequencing of the coronavirus, molecular diagnostic testing, synthetic biology, and vaccines; the digitalization of work, play, entertainment, shopping, and payments; automation, energy storage, and artificial intelligence to overcome labor shortages and supply chain bottlenecks; and blockchain technology to lower costs and increase yields on financial assets. In other words, the coronavirus crisis accelerated the adoption rate of innovation, pushing various technologies further along their S-curves[8] than otherwise would have been the case. Innovation typically solves problems. Russia’s invasion of Ukraine and China’s zero COVID policy have created even more problems for new technologies to solve.

As the coronavirus subsided, we believe short-term oriented investors began to focus on the tough comparisons that innovative companies would face against the growth rates they enjoyed during the crisis. As a result, they took profits and shifted into the momentum building behind cyclical stocks as the global economy went back to work. We kept our focus on the growth that companies focused on disruptive innovation are likely to deliver––at the expense of many traditional cyclicals and value stocks––during the next five years. Based on the performance of ARKK during the past 15 months and a global economy that now seems to be sliding into recession, perhaps deflation, this rotation now seems long in the tooth, if not overdone. In our view, true growth is likely to become “scarce” during the next few years.

According to Bloomberg’s analyst estimates and as shown below, ARKK company revenues[9] will increase 25-27% at an annual rate during the next three years which, while below ARK analysts’ expectations, still would be substantially above the revenue growth of companies in the broad-based benchmarks.[10] In contrast, from 2000 to 2002 the Nasdaq 100’s revenue growth decelerated from the low- to mid-30% range into negative territory before recovering to the low- to mid-teens in 2004-05.

Source: ARK Investment Management LLC, Bloomberg, Company Filings Notes: Excludes 2 names in ARKK[11] As of March 2022.

Forecasts are inherently limited and cannot be relied upon. For informational purposes only and should not be considered investment advice, or a recommendation to buy, sell or hold any particular security.

Given this dichotomy, we wonder why ARKK’s chart pattern today resembles that of the Nasdaq as the tech and telecom bubble was bursting in 2000-2001. While consensus expectations could be wrong, last quarter’s guidance during earnings calls seemed to suggest that revenue growth for many of our companies will accelerate in the second half of the year now that they are cycling through their toughest comparisons. Interest rates, which were declining during the tech and telecom bust in 2000-2001 but are rising now, could be another reason for ARKK’s recent performance. Yet, as measured by the ten-year Treasury yield,[12] today’s ~3% is ~45% below the 5.5% average from 2000 to 2001 while the Nasdaq 100’s trailing twelve-month (TTM) PE ratio[13] as of May 2022, is roughly 26x, a fifth of its 132x average TTM PE ratio in 2001. In other words, the discount rate is much lower today, pushing the present value of future cash flows much higher than would have been the case during the tech and telecom bust. Given the global recession that seems to be unfolding, we would be surprised to see the ten-year Treasury bond yield drift much above 3%. Indeed, given the supply chain-related surge in inflation to 40-year highs, we have been struck that the bond yield has had trouble increasing beyond 3%. The bond market seems to be telegraphing that this surge in inflation is temporary.

During the 2000-2003 bust, according to our research, roughly 25% of the companies in the Nasdaq 100 suffered declines in revenue on a year-over-year basis, some by more than 70%. Their technologies were not ready for prime time and their costs were prohibitive. Thus far, among ARKK’s 35 names,[14] only Intellia, representing ~3% of names in the portfolio, has seen its revenues decline. That said, Intellia is a pre-revenue company with what we believe is a solid patent position in the gene-editing space and, dependent on milestone payments, is investing heavily in research and development in the quest to cure diseases. During the early 2000’s, scientists had neither the funds nor the technology to identify mutations, let alone cure disease.

In fact, most companies in the Nasdaq 100 at the beginning of the millennium disappeared in mergers, acquisitions, private equity buyouts, and bankruptcies during the next fifteen years. According to our research, the acquisitions typically took place at steep discounts for companies either past their prime or before their time––among them, Sun Microsystems, I2 Technologies, and Applied Microcircuits––at valuations 10% or less of their peak market caps.

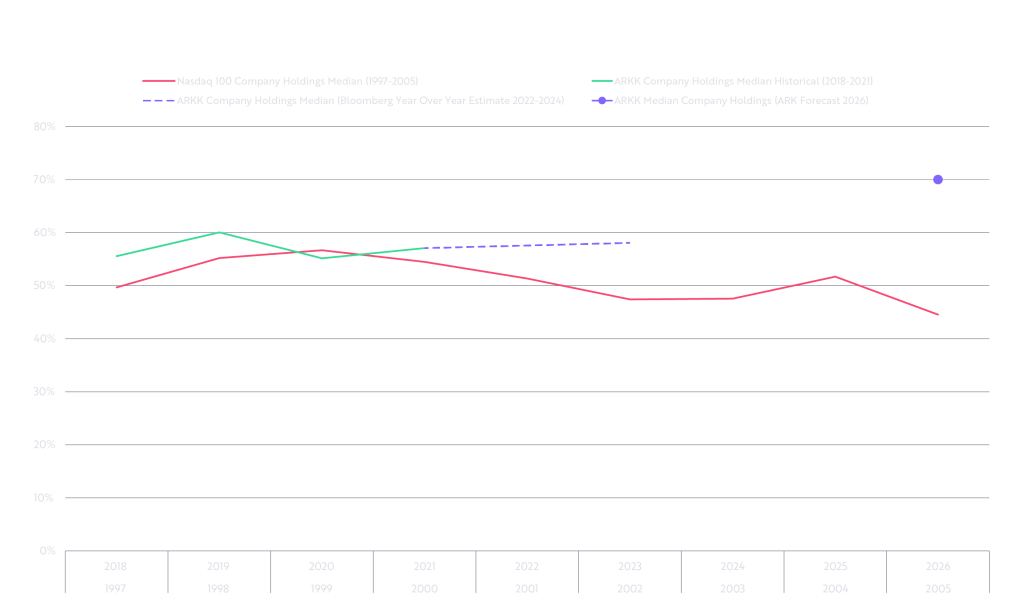

Clearly, increasing revenue does not translate necessarily into profits but, in ARKK’s case, even Bloomberg consensus estimates suggest that its companies will be increasingly profitable during the next few years, as shown below. Leading into its peak performance in 2021, ARKK companies’ median gross margin[15] increased and surpassed the Nasdaq 100’s 54.5% peak circa 2000. During the next few years, if ARKK companies’ revenue growth rates do diverge from the Nasdaq 100’s during the 2000-2003 bust, so should its relative profitability. From 2000 through 2003, the Nasdaq 100 companies’ declining profitability was the result of too much capital chasing too few opportunities too soon, suggesting that profitability trends in the broader based Nasdaq must have been much worse. From 2021 through 2024, if its company gross margins were to increase in line with Bloomberg’s consensus expectations, ARKK comparisons to the Nasdaq in the tech and telecom bust will break down, forcing the bears to rethink ARKK’s trajectory.

Source: ARK Investment Management LLC, Bloomberg, Company Filings Notes. As of March 2022. Eight (8) companies were excluded from the analysis since they are not in a stage where gross margin is a meaningful portion of the company’s value.

Forecasts are inherently limited and cannot be relied upon. For informational purposes only and should not be considered investment advice, or a recommendation to buy, sell or hold any particular security.

VALUATION: 2000-2001 vs 2021-2022

The screen for our stock selection is not a benchmark: it is our analysts’ substantive, rigorous research specialized by technology. We focus on the right technology at the right time, placing emphasis on companies investing aggressively today and sacrificing short-term profitability to capitalize on exponential growth opportunities, many of them in the “winner take most” category thanks to breakthroughs in deep learning, computing power, networking, and energy storage. As a result, while ARKK’s current companies’ TTM PE, Enterprise Value (EV)[16] to Sales, and EBITDA[17] ratios are high at ~70x, 9.3x, and 69x, respectively, our revenue and EBITDA growth expectations are 59% and 87%,[18] respectively, during the next five years. We do assume that by year five our companies will be harvesting cash flow as they approach “end-of-life” liquidity events like acquisitions. That said, one of the characteristics of companies capitalizing on our five innovation platforms is that they are launching pads for more innovation. If our companies are not preparing for liquidity events, and most of them will not be, they probably will continue to sacrifice short-term profitability to invest in the next leg of their innovation strategies.

To derive our price targets, we make the important assumption that multiples will compress toward the mid-to-high teens on an EV/EBITDA basis during the next five years. For perspective, the Nasdaq 100’s TTM EV/EBITDA ratio today is 15.7x, not far from the ratio we project for our strategies in five years. As a result, multiple compression[19] from 69x to 15.7x is a headwind in our forecast assumptions, not the steady state most strategists expect in their forecasts.

The performance of our strategies relies importantly on our companies’ exponential revenue and EBITDA growth trajectories. Their exponential growth, in turn, is a function of Wrights Law[20] applied to each technology, and each technology’s potential to scale across sectors, serving as launching pads for more innovation. As the technologies converge with one another, S-curves feeding S-curves, multiplicative or combinatorial forces could turbocharge growth rates. According to our research, for example, the convergence between and among robotics, energy storage, and artificial intelligence will create $9-10 trillion revenue and $30-50 trillion equity market cap opportunities in 2030, while genomic sequencing, artificial intelligence, and gene editing converge to cure diseases – seemingly creating priceless opportunities – could create more than $3 trillion in enterprise value. In our opinion, investors with a short-term focus, or those focused on tried-and-true winners, probably are not prepared to measure the impact and ripple effects of these convergences in a world of unprecedented technological transformation.

CONCLUSION

ARK believes that the best set-up for above average returns over the long term is to invest contrary to consensus thinking, and to be right. ARKK’s spurious correlation to the Nasdaq during the tech and telecom bust, and the unusually strong correlation among technologies that are developing independently, have increased our confidence that the markets today are behaving irrationally and illogically. Given the collapse in ARKK’s price and the fear in markets as measured by cash levels, we have very high conviction in our bets against consensus thinking, stemming from our first-principles research.

ARK publishes its research online, among other reasons to highlight transformational technologies that will disrupt every economic sector globally. Exceedingly loose fiscal and monetary policies didn’t sequence the coronavirus and create vaccines in record time, or allow workers to collaborate seamlessly from home, or develop AI models that have boosted software engineering productivity dramatically. We believe persistent supply chain problems and Russia’s invasion of Ukraine have created more problems that will accelerate the adoption of innovation, increase productivity, and turn the tide from higher inflation and interest rates to lower inflation, if not deflation, and interest rates. As we have stated time and time again, innovation solves problems and rarely has the world confronted as many challenges as it faces today.

Important Information

Past performance does not guarantee future results.

ARK’s actively managed ETFs are benchmark agnostic. Index performance provided as a general market indicator. Indexes are unmanaged. It is not possible to invest directly in an index.

Investors should carefully consider the investment objectives and risks as well as charges and expenses of an ARK ETF before investing. This and other information are contained in the ARK ETFs’ prospectuses, which may be obtained by visiting www.ark-funds.com. The prospectus should be read carefully before investing.

An investment in an ARK ETF is subject to risks and you can lose money on your investment in an ARK ETF. There can be no assurance that the ARK ETFs will achieve their investment objectives. The ARK ETFs’ portfolios are more volatile than broad market averages. Additional risks of investing in ARK ETFs include equity, market, management, and non-diversification risks, as well as fluctuations in market value and NAV. The ETF’s portfolio is more volatile than broad market averages. Shares of ARK ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the ETF. ETF shares may only be redeemed directly with the ETF at NAV by Authorized Participants, in very large creation units. There can be no guarantee that an active trading market for ETF shares will develop or be maintained, or that their listing will continue or remain unchanged. Buying or selling ETF shares on an exchange may require the payment of brokerage commissions and frequent trading may incur brokerage costs that detract significantly from investment returns.

The principal risks of investing in the ARK ETFs include: Equity Securities Risk. The value of the equity securities the ARK ETF holds may fall due to general market and economic conditions. Foreign Securities Risk. Investments in the securities of foreign issuers involve risks beyond those associated with investments in U.S. securities. Disruptive Innovation Risk. Companies that ARK believes are capitalizing on disruptive innovation and developing technologies to displace older technologies or create new markets may not in fact do so. Companies that initially develop a novel technology may not be able to capitalize on the technology. Companies that develop disruptive technologies may face political or legal attacks from competitors, industry groups or local and national governments. These companies may also be exposed to risks applicable to sectors other than the disruptive innovation theme for which they are chosen, and the securities issued by these companies may underperform the securities of other companies that are primarily focused on a particular theme. Special Purpose Acquisition Companies (SPAC) Risk. A SPAC is a publicly traded company that raises investment capital for the purpose of acquiring or merging with an existing company. Investments in SPACs and similar entities are subject to a variety of risks beyond those associated with other equity securities. Because SPACs and similar entities do not have any operating history or ongoing business other than seeking acquisitions, the value of their securities is particularly dependent on the ability of the SPAC’s management to identify a merger target and complete an acquisition. The ARK ETFs also have specific principal investment risks, which are described below. More detailed information regarding these risks can be found in the ARK ETFs’ prospectuses.

Aerospace and Defense Company Risk. Companies in the aerospace and defense industry rely to a large extent on U.S. (and other) Government demand for their products and services and may be significantly affected by changes in government regulations and spending, as well as economic conditions, industry consolidation and other disasters.

Biotechnology Company Risk. A biotechnology company’s valuation can often be based largely on the potential or actual performance of a limited number of products and can accordingly be greatly affected if one of its products proves, among other things, unsafe, ineffective, or unprofitable. Biotechnology companies are subject to regulation by, and the restrictions of, the U.S. Food and Drug Administration, the U.S. Environmental Protection Agency, state and local governments, and foreign regulatory authorities.

Communications Sector Risk. Companies is this sector may be adversely affected by potential obsolescence of products/services, pricing competition, research and development costs, substantial capital requirements and government regulation.

Consumer Discretionary Risk. Companies in this sector may be adversely impacted by changes in domestic/international economies, exchange/interest rates, social trends, and consumer preferences.

Cryptocurrency Risk. Cryptocurrency (notably, bitcoin), often referred to as ‘‘virtual currency’’ or ‘‘digital currency,’’ operates as a decentralized, peer-to-peer financial exchange and value storage that is used like money. The Fund may have exposure to bitcoin, a cryptocurrency, indirectly through an investment in the Bitcoin Investment Trust (‘‘GBTC’’), a privately offered, open-end investment vehicle. Cryptocurrency operates without central authority or banks and is not backed by any government. Even indirectly, cryptocurrencies may experience very high volatility and related investment vehicles like GBTC may be affected by such volatility. As a result of holding cryptocurrency, the Fund may also trade at a significant premium to NAV. Cryptocurrency is also not legal tender. Federal, state, or foreign governments may restrict the use and exchange of cryptocurrency, and regulation in the U.S. is still developing. Cryptocurrency exchanges may stop operating or permanently shut down due to fraud, technical glitches, hackers, or malware. Many significant aspects of the U.S. federal income tax treatment of investments in bitcoin are uncertain and an investment in bitcoin may produce income that is not treated as qualifying income for purposes of the income test applicable to regulated investment companies, such as the Fund. GBTC is expected to be treated as a grantor trust for U.S. federal income tax purposes, and therefore an investment by the Fund in GBTC will generally be treated as a direct investment in bitcoin for such purposes. See ‘‘Taxes’’ in the Fund’s SAI for more information.

Financial Technology Risk. Companies that are developing financial technologies that seek to disrupt or displace established financial institutions generally face competition from much larger and more established firms. Fintech Innovation Companies may not be able to capitalize on their disruptive technologies if they face political and/or legal attacks from competitors, industry groups or local and national governments. Blockchain technology is new and many of its uses may be untested. Blockchain and Digital commodities and their associated platforms are largely unregulated, and the regulatory environment is rapidly evolving. As a result, companies engaged in such blockchain activities may be exposed to adverse regulatory action, fraudulent activity or even failure.

Health Care Sector Risk. The health care sector may be adversely affected by government regulations and government health care programs, restrictions on government reimbursements for medical expenses, increases or decreases in the cost of medical products and services and product liability claims, among other factors. Many health care companies are heavily dependent on patent protection and intellectual property rights and the expiration of a patent may adversely affect their profitability.

Industrials Sector Risk. Companies in the industrials sector may be adversely affected by changes in government regulation, world events and economic conditions. In addition, companies in the industrials sector may be adversely affected by environmental damages, product liability claims and exchange rates.

Information Technology Sector Risk. Information technology companies face intense competition, have limited product lines, markets, financial resources, or personnel, face rapid product obsolescence, are heavily dependent on intellectual property and the loss of patent, copyright and trademark protections may adversely affect the profitability of these companies.

Pharmaceutical Company Risk. Companies in the pharmaceutical industry can be significantly affected by, among other things, government approval of products and services, government regulation and reimbursement rates, product liability claims, patent expirations and protection and intense competition.

Certain of the statements contained in this presentation may be statements of future expectations and other forward-looking statements that are based on ARK’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied in such statements. The matters discussed in this presentation may also involve risks and uncertainties described from time to time in ARK’s filings with the U.S. Securities and Exchange Commission. ARK assumes no obligation to update any forward-looking information contained in this presentation. ARK and its clients as well as its related persons may (but do not necessarily) have financial interests in securities or issuers that are discussed. Certain information was obtained from sources that ARK believes to be reliable; however, ARK does not guarantee the accuracy or completeness of any information obtained from any third party.

Index Descriptions:

The S&P 500® Index is a widely recognized capitalization-weighted index that measures the performance of the large-capitalization sector of the U.S. stock market.

The NASDAQ-100 Index is a stock market index that includes 100 of the largest, most actively traded, non-financial companies that are listed on the Nasdaq Stock Market.

The NASDAQ Composite is a stock market index that includes almost all stocks listed on the Nasdaq stock exchange. Along with the Dow Jones Industrial Average and S&P 500, it is one of the three most-followed stock market indices in the United States.

ARK ETFs are distributed by Foreside Fund Services, LLC.

©2021-2026, ARK Investment Management LLC. No part of this material may be reproduced in any form, or referred to in any other publication, without the express written permission of ARK Investment Management LLC (“ARK”).

Source – https://ag.ny.gov/sites/default/files/press-releases/archived/MerrillL.pdf, As of April 2002.

Source – BofA Global Fund Manager Survey, April 2022.

This time span was chosen as it represents the years leading up to the ARKK/Nasdaq’s peaks through the following 5-year period.

Generative Pre-trained Transformer 3 is an autoregressive language model that uses deep learning to produce human-like text. It is the third-generation language prediction model in the GPT-n series created by OpenAI, a San Francisco-based artificial intelligence research laboratory.

Source – BofA Global Fund Manager Survey, February 2022.

Source – Bloomberg, May 2022.

The S-curve shows the innovation from its slow early beginnings as the technology or process is developed, to an acceleration phase (a steeper line) as it matures and, finally, to its stabilization over time (the flattening curve), with corresponding increases in performance of the item or organization using it.

Data as of March 2022. Portfolio holdings and allocations are subject to change and should not be considered investment advice or a recommendation to buy, sell or hold any particular security.

Data as of March 2022. Broad-based benchmarks in this instance is defined as companies within the S&P 500 and the NASDAQ 100 where corresponding Bloomberg analyst estimates were sourced from.

Two names excluded due to the volatility of milestone revenue causing a distorted revenue picture. Data as of March 2022.

The 10-year Treasury yield is the yield that the government pays investors that purchase the specific security. Purchase of the 10-year note is essentially a loan made to the U.S. government.

P/E is price to earnings ratio, used as a valuation metric by comparing a company’s current price to its earnings per share. Trailing 12 months is the time frame to use for calculating the earnings.

As of March 31, 2022. Please see the most up to date holdings for ARKK at: https://ark-funds.com/funds/arkk/. Portfolio holdings and allocations are subject to change and should not be considered investment advice or a recommendation to buy, sell or hold any particular security.

Median is the central number of a data set. Gross Margin is net sales minus the cost of goods sold. Typically can be found as a percent of revenue.

Enterprise value (EV) is a measure of a company’s total value, often used as a more comprehensive alternative to equity market capitalization. Enterprise value includes in its calculation the market capitalization of a company but also short-term and long-term debt as well as any cash on the company’s balance sheet.

EBITDA is an acronym meaning Earnings Before Interest, Taxes, Depreciation, and Amortization.

Data is as of May 2022.

Multiple compression occurs when a company’s earnings increase faster than its price. The result would be a lower price to earnings multiple.

ARK’s statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. ARK and its clients as well as its related persons may (but do not necessarily) have financial interests in securities or issuers that are discussed. Certain of the statements contained may be statements of future expectations and other forward-looking statements that are based on ARK’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied in such statements.

ARK Trade Notifications

ARK offers fully transparent Exchange Traded Funds (“ETFs”) and provides investors with trade information for all actively managed ETFs.