MACRO BACKDROP

Unsettled global markets in the first quarter of 2026 echoed those during the first quarter of 2025. As was the case last year, innovation-oriented equities underperformed broader benchmarks, with the ARK Innovation ETF (ARKK) declining 12.22%, compared to the ~4% and ~6% declines in the S&P 500 and Nasdaq 100 Indexes, respectively, benchmarks more heavily weighted toward mega-cap incumbents than pure-play innovation exposures. Last year’s tariff escalation and policy uncertainty weighed heavily on sentiment and disrupted market momentum. This year, geopolitical tensions, including the war in Iran, reintroduced fears of higher inflation and weaker global growth.

While recent inflation data continue to spark concerns, the underlying trajectory seems more nuanced, particularly because producer price inflation is higher than consumer price inflation. Alternative real-time consumer price metrics from Truflation1 suggest that inflation has dropped and remains below government measures, as the deflationary undercurrents associated with technological progress—AI, robotics, energy storage, and other innovation platforms—are pressuring costs. At the same time, the Federal Reserve’s dual mandate brings labor market dynamics into sharper focus. Signs of employment weakness, particularly among recent college graduates, could reflect AI-driven productivity shifts, baby-boom retirements, and a drop in immigration, among other forces. Geopolitical pressures, including those linked to Iran, could exacerbate the near-term volatility in inflation, though notably core inflation2 as measured by Truflation has decelerated to 1.72% as of March 31, 2026.

Other sources of market volatility during the first quarter included a reassessment of AI, hyperscaler3 capital expenditures, and value distribution across the software ecosystem, all of which aggravated fourth-quarter concerns about the dislocations that frontier AI models are causing. That dynamic—also called “SaaSpocalypse”—ignited a broad repricing of software and Software as a Service (SaaS)-related equities as investors confronted the possibility that AI platforms, agents, and usage-based models could disrupt traditional seat-based software economics more rapidly than anticipated. Breakthroughs from leading model providers highlighted how quickly they might automate knowledge work, ultimately challenging the economic foundations of seat-based software. While the advancements are validating the scale and speed of the platform shifts now underway, in our view the market response was indiscriminate—de-risking of anything perceived as “software”—overlooking the companies aligned with AI and enabling the AI transition.

PERFORMANCE

The ARK Venture Fund (Class D) returned 5.29% during the quarter, outperforming the S&P 500 and MSCI World Index, which fell 4.33% and 3.47%, respectively.

The top contributors to performance were SpaceX and Replit, both of which benefited from valuation step-ups during the quarter, reflecting strong investor demand for category-defining companies aligned with long-term innovation themes. Replit’s re-rating followed a new funding round that underscored accelerating adoption of AI-powered software development tools, while SpaceX’s valuation appreciation was driven by its merger with xAI, continued strength in secondary markets, and growing anticipation of a potential public offering. As public markets stabilized and liquidity expectations improved, private market leaders with scale, revenue traction, and strategic importance were re-rated higher.

Shares of SpaceX continued to benefit from its dominant position in launch services and satellite communications, further reinforced by sustained investor demand and confidence in Starlink’s revenue trajectory and long-term cash flow potential. Its combination with xAI further strengthens its strategic positioning at the intersection of connectivity and artificial intelligence.

On February 2, 2026, SpaceX announced the acquisition of xAI, advancing the convergence of launch, energy, and artificial intelligence into a single, vertically integrated platform. In our view, one of the most important bottlenecks constraining AI today is access to abundant, low-cost power. By integrating launch capabilities with energy and AI model development, SpaceX could be attempting to transcend terrestrial constraints, potentially enabling a new paradigm for compute infrastructure.

If Starship achieves full reusability and drives launch costs below $100 per kilogram, we believe orbital data centers powered by space-based energy could become economically competitive with—and potentially ~25% less expensive than—terrestrial alternatives at scale. Such a shift could reconfigure the cost curve for AI, accelerating deployment while expanding access to increasingly powerful models.

In our view, the SpaceX–xAI combination positions the company to control a critical chokepoint in the AI value chain: scalable, cost-efficient compute. Historically, ownership of key infrastructure layers has defined technological leadership across major innovation platforms. We believe the convergence of aerospace, energy, and AI could follow a similar pattern.

Importantly, our current valuation framework for SpaceX is driven primarily by our expectations for Starlink and does not include contributions from orbital data centers. As a result, we believe our base case may not fully reflect the potential upside associated with this emerging opportunity.

Shares of Replit contributed significantly as well, following its capital raise, which highlighted strong demand for AI-native developer platforms. The company’s rapid user growth and monetization of AI-assisted coding tools position it as a leading platform in the evolving software development stack, benefiting from the broader shift toward automation and productivity enhancement.

Together, these companies exemplify how, even amid macro uncertainty, capital continues to concentrate in a narrow set of innovation leaders with large addressable markets that are accelerating adoption curves and improving unit economics, dynamics that supported ARKVX’s relative performance during the quarter.

The top detractors from performance were Kodiak AI and Lambda.

Shares of Kodiak AI detracted from fund performance during the quarter, trading below its October 2025 IPO price, as the market digested the company's pre-revenue profile and capital requirements. Despite the share price weakness, Kodiak continued to demonstrate meaningful operational progress: the company doubled its fleet of fully driverless trucks to 20, surpassed 10,700 cumulative hours of paid driverless operations, and announced a strategic collaboration with Bosch to develop a production-grade autonomous platform for scaling its AI-powered driver to commercial trucks. On the defense side, the U.S. Marine Corps awarded Kodiak a contract to integrate its autonomous driver into the ROGUE-Fires expeditionary vehicle, and the company unveiled the Leonidas Autonomous Ground Vehicle in partnership with Epirus and General Dynamics for counter-UAS missions. Management reiterated its target to launch driverless long-haul trucking by late 2026.

Shares of Lambda faced pressure during the quarter as infrastructure providers in the artificial intelligence ecosystem experienced increased investor scrutiny around capital intensity, competitive dynamics, and the pace of monetization. While demand for AI compute remains strong, valuation multiples across the space compressed modestly as investors recalibrated expectations around near-term margins and the timing of returns on large-scale infrastructure investments. Despite those headwinds, Lambda continues to expand its GPU cloud footprint and deepen enterprise adoption, positioning it as a key enabler of AI development.

ACTIVE MANAGEMENT

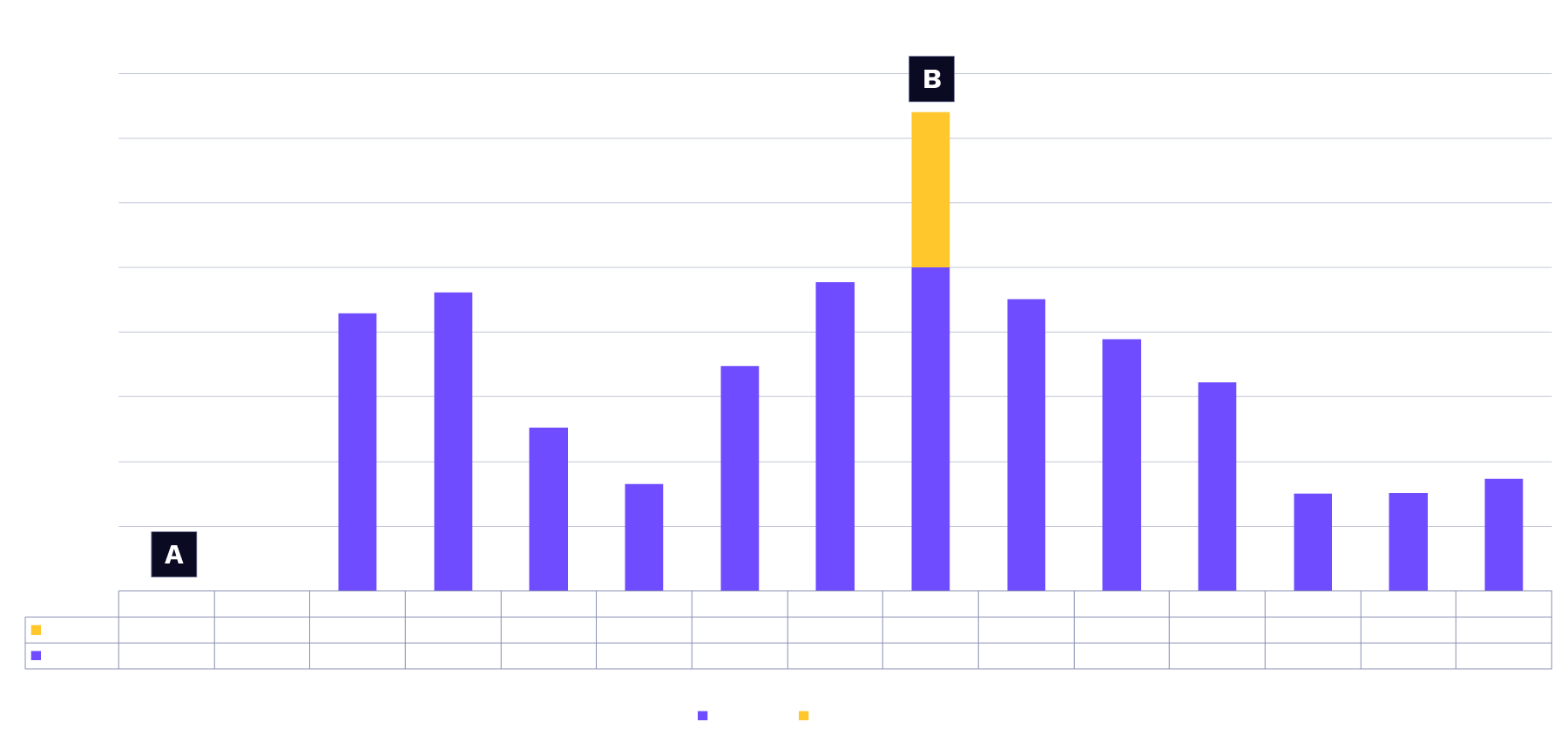

During the quarter, the ARK Venture Fund’s assets under management (AUM) increased from $491 million to $711 million, thanks to market appreciation and $207 million of net inflows.

New Positions

We deployed that capital to initiate new positions in Crusoe (Private), Roblox (RBLX), and Shopify (SHOP).

- Crusoe is an energy-first AI infrastructure company building scalable, sustainable computing platforms that power next-generation artificial intelligence workloads. Crusoe’s vertically integrated approach combines innovative energy solutions with high-performance data center design, harnessing otherwise wasted or clean energy to deliver reliable, cost-effective AI compute at scale and reduce the environmental impact of traditional cloud providers. Trusted by leading technology partners and supported by long-duration capital, Crusoe enables enterprises and developers to accelerate AI innovation with robust cloud services and modular data center infrastructure.

- Roblox is an online entertainment platform that enables users to engage with a variety of virtual worlds and experiences created by independent developers. With over 80 million daily active users and a flexible, easy-to-use development environment in Roblox Studio, we believe the company is well-positioned to emerge as the de-facto leader in user-generated content and indie entertainment platforms. As generative AI collapses the cost and time required to create 3D content, Roblox’s proprietary data advantages and massive creator ecosystem should accelerate adoption dramatically, merging the roles of user and developer. With continued consumer adoption of AR and VR devices, Roblox also could become a primary platform for digital socialization globally, positioning it at the intersection of ARK’s Neural Networks and Intelligent Devices technology platforms.

- Shopify is a comprehensive omnichannel e-commerce platform that enables merchants to design, set up, and manage their stores across multiple sales channels, equipping them with payment processing, shipping, customer engagement tools, and more. Increasingly, Shopify is positioned as the operating system for independent commerce, and its native support for Model Context Protocol (MCP) endpoints enables its merchants to feed product and inventory data directly into the agentic web—a critical advantage as AI purchasing agents reshape how consumers discover and buy products online. Recent integrations with OpenAI and Lovable have lowered the barriers to entrepreneurship, cutting the time from idea to live storefront from weeks to minutes.

Increased Positions

We also added to existing positions in Lucra, Databricks, SpaceX, Replit, Ayar Labs, and OpenAI, maintaining approximately 80% exposure to private companies, as shown below.

Source: ARK Investment Management LLC 2026, based on data as of 12/31/25. The data presented is for informational purposes only. Total assets under management (AUM) and allocation breakdown are subject to change. Historical increases in AUM are not a guarantee of future increases as AUM may decrease during down markets and/or as the result of redemptions.

Initial Public Offerings (IPOs)

Generate:Biomedicines IPO’d during the quarter. Generate:Biomedicines is a clinical-stage generative biology company that uses its proprietary AI platform to design protein therapeutics with specified biological intent, engineering molecules with differentiated clinical profiles that traditional discovery methods struggle to achieve. The company's lead asset, GB-0895, is a long-acting anti-TSLP antibody engineered for potential every-six-month dosing, now in Phase 3 for severe asthma, offering a meaningful dosing advantage over existing monthly biologics that could unlock significantly higher treatment adoption. We believe Generate represents a convergence of ARK's core AI and multiomics investment themes, with a therapeutic-area and modality-agnostic platform that repeatedly can generate differentiated drug candidates across immunology, oncology, and beyond.

Liquidity Management

The Fund offers quarterly liquidity at the end of each calendar quarter. Approximately three to four weeks prior to each redemption deadline, the Fund (1) proactively accumulates up to ~5% cash to meet anticipated liquidity needs, (2) reserves capital for near-term private investments, and (3) allocates the remainder to public equities. This approach seeks to minimize taxable transactions and avoid forced selling of public positions.

Source: ARK Investment Management LLC. As of December 31, 2025. The data presented is for informational purposes only.

As of March 31, 2026, redemption requests totaled $12.3 million, or 1.7% of the Fund, which were fully covered by cash accumulated prior to quarter end.

Source: ARK Investment Management LLC. As of December 31, 2025. Past grants of liquidity is not a guarantee of future liquidity. The data presented is for informational purposes only.

OUTLOOK

Looking ahead, the constructive signals we began to observe at the end of 2025 have continued into the first quarter of 2026, reinforcing our view that the IPO market is likely to reopen selectively rather than broadly. While capital markets appear increasingly receptive to scaled, high-quality innovation platforms, we believe the bar for public entry remains elevated, favoring companies with strong revenue growth, clear paths to profitability, and differentiated technology positions.

In our view, this more disciplined environment is a healthy development. Rather than rewarding speculative business models, public investors seem to be prioritizing companies demonstrating measurable traction, capital efficiency, and durable competitive advantages. As a result, we believe the next wave of IPOs is likely to be led by companies that have already achieved significant scale in private markets and are seeking access to public capital to accelerate, not validate, their growth.

Within this context, innovation-driven sectors continue to mature rapidly. AI-native platforms across foundational models, enterprise applications, and developer ecosystems are scaling at unprecedented rates, in some cases reaching multi-billion-dollar revenue run rates within a few years of inception. At the same time, infrastructure-oriented platforms spanning connectivity, compute, and data are becoming increasingly critical to enabling the next phase of AI deployment, with several approaching levels of operational scale and resilience consistent with public-market expectations.

While uncertainty around timing persists, particularly given macroeconomic and policy dynamics, we believe the pipeline of potential issuers remains robust. Importantly, we continue to view the public markets not as an endpoint, but as a critical milestone in the lifecycle of disruptive innovation platforms, providing liquidity, transparency, and access to capital to support continued exponential growth.

More broadly, in our view, markets will continue climbing the wall of worry created by geopolitical uncertainty, evolving monetary policy expectations, and ongoing reassessments of the impact of artificial intelligence. Developments in the Middle East could continue to influence energy markets and inflation expectations, while central banks remain committed to driving policy based on data. Investors continue to assess the balance between near-term AI capital intensity and longer-term productivity gains—crosscurrents that are likely to sustain debate, market volatility, and dispersion among equity strategies.

In our view, this environment is fertile ground for long-term investors. Periods marked by uncertainty tend to create “walls of worry” that sustain bull markets. The current wall of worry reflects a market digesting a major technology platform shift—not one nearing exhaustion. The repricing across software, compute infrastructure, and adjacent sectors is a function of identifying areas of value accrual in an AI-driven economy.

Important Information

Investors should carefully consider the ARK Venture Fund's investment objectives and risks, as well as charges and expenses, before investing. This and other information are contained in the ARK Venture Fund’s prospectus, which may be obtained by visiting www.ark-funds.com.

The ARK VENTURE FUND is a continuously-offered, non-diversified, registered closed-end fund with limited liquidity. An investment in the Fund’s Shares is not suitable for investors that require liquidity, other than liquidity provided through the Fund’s repurchase policy.

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal will fluctuate so that an investor’s shares when redeemed may be worth more or less than the original cost. For the Fund’s most recent month-end and standardized performance, please visit www.ark-funds. com/funds/arkvx or call 1-800-679-7759

All statements made regarding investment opportunities are strictly beliefs and points of view held by ARK and investors should determine for themselves whether a particular investment or service is suitable for their investment needs. Certain statements contained in this document may be statements of future expectations and other forward-looking statements that are based on ARK’s current views and assumptions, and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. The matters discussed in this document may also involve risks and uncertainties described from time to time in ARK’s filings with the U.S. Securities and Exchange Commission. ARK assumes no obligation to update any forward-looking information contained in this document.

ARK assumes no obligation to update any forward-looking information contained in this document.

You should not expect to be able to sell your Shares other than through the Fund’s repurchase policy, regardless of how the Fund performs. The Fund’s Shares will not be listed on any securities exchange, and the Fund does not expect a secondary market in the Shares to develop. Shares may be transferred or sold only in accordance with the Fund’s prospectus. Although the Fund will offer to repurchase Shares on a quarterly basis, Shares are not redeemable and there is no guarantee that shareholders will be able to sell all of their tendered Shares during a quarterly repurchase offer. An investment in the Fund’s Shares is not suitable for investors that require liquidity, other than liquidity provided through the Fund’s repurchase policy.

There is no assurance that the Fund will meet its investment objective. The value of your investment in the Fund, as well as the amount of return you receive on your investment in the Fund, may fluctuate significantly. You may lose part or all of your investment in the Fund or your investment may not perform as well as other similar investments. Therefore, you should carefully consider the following risks before investing in the Fund.

Principal Risks of the Fund Include:

Private Company Risk. The Fund invests in private, early-stage companies that may be considered highly speculative. As a result, investment in shares of the Fund involves substantial risks including risks associated with uncertainty regarding the valuations of private company investments, high rate of failure among the early-stage companies, and restricted liquidity in securities of such companies. Communications Sector Risk. The Fund will be more affected by the performance of the communications sector than a fund with less exposure to such sector. Cyber Security Risk. As the use of Internet technology has become more prevalent in the course of business, funds have become more susceptible to potential operational risks through breaches in cyber security. Disruptive Innovation Risk. Companies that the Adviser believes are capitalizing on disruptive innovation and developing technologies to displace older technologies or create new markets may not in fact do so. Financial Technology Risk. Companies that are developing financial technologies that seek to disrupt or displace established financial institutions generally face competition from much larger and more established firms. Next Generation Internet Companies Risk. The risks described below apply, in particular, to the Fund’s investment in Next Generation Internet Companies.

Foreign Securities Risk. The Fund’s investments in foreign securities can be riskier than U.S. securities investments. Investments in the securities of foreign issuers (including investments in ADRs and GDRs) are subject to the risks associated with investing in those foreign markets, such as heightened risks of inflation or nationalization. The prices of foreign securities and the prices of U.S. securities have, at times, moved in opposite directions. In addition, securities of foreign issuers may lose value due to political, economic and geographic events affecting a foreign issuer or market. During periods of social, political or economic instability in a country or region, the value of a foreign security traded on U.S. exchanges could be affected by, among other things, increasing price volatility, illiquidity, or the closure of the primary market on which the security (or the security underlying the ADR or GDR) is traded. You may lose money due to political, economic and geographic events affecting a foreign issuer or market. The Fund normally will not hedge any foreign currency exposure. Future Expected Genomic Business Risk. The Adviser may invest some of the Fund’s assets in Genomics Revolution Companies that do not currently derive a substantial portion of their current revenues from genomic-focused businesses and there is no assurance that any company will do so in the future, which may adversely affect the ability of the Fund to achieve its investment objective. Emerging Market Securities Risk. Investment in securities of emerging market issuers may present risks that are greater than or different from those associated with securities of developed market issuers due to less developed and liquid markets and such factors as increased economic, political, regulatory, or other uncertainties.

Cryptocurrency Risk. Cryptocurrencies (also referred to as “virtual currencies” and “digital currencies”) are digital assets designed to act as a medium of exchange. Cryptocurrency is an emerging asset class. There are thousands of cryptocurrencies, the most well-known of which is bitcoin. The Fund may have exposure to cryptocurrencies, such as bitcoin indirectly through an investment in the Bitcoin Investment Trust (“GBTC”), a privately offered, open-end investment vehicle that invests in bitcoin. Health Care Sector Risk. The health care sector may be affected by government regulations and government health care programs, restrictions on government reimbursement for medical expenses, increases or decreases in the cost of medical products and services and product liability claims, among other factors. Leverage Risk. The use of leverage can create risks. Leverage can increase market exposure, increase volatility in the Fund, magnify investment risks, and cause losses to be realized more quickly. Non-Diversification Risk. The Fund is classified as a “non-diversified” investment company under the 1940 Act. Therefore, the Fund may invest a relatively higher percentage of its assets in a relatively smaller number of issuers or may invest a larger proportion of its assets in a single issuer. As a result, the gains and losses on a single investment may have a greater impact on the Fund’s NAV and may make the Fund more volatile than more diversified funds.

To view the top 10 holdings in the ARK Venture Fund, click here. To view the most up-to-date portfolio, click here.

An investment in the ARK Venture Fund is subject to risks, and you can lose money on your investment. There can be no assurance that the ARK Venture Fund will achieve its investment objectives. The ARK Venture Fund’s portfolio is more volatile than broad market averages. The ARK Venture Fund also has specific risks, which are described below. More detailed information regarding these risks can be found in the ARK Venture Fund’s prospectus.

Diversification neither assures a profit nor guarantees against loss in a declining market.

“OB3” or the “One Big Beautiful Bill Act,” is a U.S. federal statute passed by Congress containing tax and spending policies that form the core of President Donald Trump's second-term agenda.

“Rolling Recession” refers to a type of recession that affects different sectors of the economy at different times—not simultaneously.

Gross Domestic Product (GDP) is the total monetary or market value of all the finished goods and services produced within a country’s borders in a specific time period.

Foreside Fund Services, LLC, distributor.

ARK Investment Management LLC (“ARK Invest”) is the investment adviser to the ARK Venture Fund.

Truflation is an independent, real-time economic data provider that calculates daily inflation metrics using over 13 million data points from more than 30 sources. It offers a high-frequency alternative to traditional, slower government metrics (like CPI), designed to provide a more accurate and immediate ("true") reflection of consumer cost-of-living changes.

Core inflation is a measure of long-term price trends that excludes volatile food and energy costs from headline inflation data (CPI or PCE).

A hyperscaler is a massive-scale cloud service provider that offers computing, storage, and networking resources capable of scaling resources dynamically to meet high demands.

ARK’s statements are not an endorsement of any company or a recommendation to buy, sell or hold any security. ARK and its clients as well as its related persons may (but do not necessarily) have financial interests in securities or issuers that are discussed. Certain of the statements contained may be statements of future expectations and other forward-looking statements that are based on ARK’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied in such statements.

Explore ARK Funds

Featured Funds: